In 2016, Milliman partnered with PharmAccess Foundation, a non-government organisation (NGO) based in the Netherlands, on an analysis involving the establishment of a health insurance pricing scheme in a state in an African country. Milliman’s role in this initiative was to provide actuarial, clinical and financial review of PharmAccess’s modelling of the anticipated costs under the health insurance pricing scheme. PharmAccess’s role was to deliver advice to the state government’s Ministry of Health (MoH). Ultimately, it was the MoH’s responsibility to make final decisions on the benefit package and associated premium to charge. Through this project, Milliman brought together a strong international consulting team of actuaries, clinicians and other consultants.

About PharmAccess

PharmAccess Foundation (PharmAccess) is a not-for-profit NGO committed to improving access to quality healthcare in low-income countries in Africa through innovative financing mechanisms, state-of-the-art medical and health administrative knowledge and public-private partnerships with local organisations. Since 2001, PharmAccess has evolved from an organisation focused on HIV/AIDS treatment to a general health organisation supporting programs and services in health insurance for low-income groups, quality improvement and quality assurance of clinics and hospitals, support of corporate and national healthcare programs and clinical and operational research. PharmAccess established the Health Insurance Fund for African target populations and the Medical Credit Fund which provides affordable loans as well as clinical, business and technical assistance to clinics. PharmAccess also hosts the SafeCare Initiative to support stepwise quality improvement programs of African healthcare providers in resource-poor settings (by using International Society for Quality in Healthcare [ISQua]-approved standards).

About Milliman’s MicroAssist support to PharmAccess

In 2011, the Milliman MicroAssist Program (MAP) expressed interest in offering Milliman consultants the opportunity to provide technical assistance to PharmAccess programs. Milliman MicroAssist is a volunteer program facilitating use of consultants’ specialised skills and experience in markets that have an urgent need, extending the reach and effectiveness of Milliman’s corporate social responsibility efforts. The spectrum of expertise is complementary to the programs of PharmAccess and could improve the quality and efficiency of the provided care. Since 2011, Milliman has been involved in several MicroAssist projects for PharmAccess, including an actuarial review of a premium-model designed by PharmAccess that estimates the total costs and an actuarially fair premium for a new health insurance plan in Mozambique for the population of approximately 22,000 students and staff of the University Eduardo Mondlane (UEM). In this paper, we describe our role and challenges in the latest project on the establishment of a health insurance pricing scheme in a developing region.

Challenges of microinsurance pricing

Although there is an increasing recognition of the value of microinsurance in developing countries, health microinsurance products are still relatively new. The difficulty in pricing health microinsurance due to lack of historical data is often one of the key challenges to developing a new product. As these programs are new, health microinsurance programs typically reflect a significant amount of risk being assumed by a government entity or other funding agency. Because of the uncertainty surrounding the pricing of these products, it is important to involve actuaries and other financial professionals familiar with the risks of healthcare insurance in the development of health microinsurance products.

Obtaining appropriate population demographics and incidence rate data continues to be a major challenge in the pricing of health microinsurance programs. Typically, data regarding population demographics is more readily obtainable than historical incidence rate data for the target population; however, this can also be a challenge when there is no reliable data on the registration of citizens. In these situations, it is often necessary to estimate population demographics and incidence rates by adjusting data from other (potentially similar) populations. Using historical data from other populations also has significant challenges because the historical data will not reflect the situation of the target population. It is often necessary to adjust the data from similar populations or make assumptions using general knowledge regarding typical population demographics and health insurance incidence rates.

The significant uncertainty surrounding microinsurance populations is in contrast to the availability of data in the western world. Demographic assumptions are one of the key factors affecting the overall cost structure of new health microinsurance products. It might also be necessary to make adjustments for pent-up demand and adverse selection, both of which are subject to great uncertainty when dealing with new markets.

Ensuring procedures, investigations and drugs are coded correctly is crucial to accurate pricing. The use of a coding list is generally key to the success of an insurance scheme in order to facilitate the reporting and delivery of covered healthcare services. However, very often the use of a standard coding and pricing list is not available, especially in a digital format.

It is also important to determine which benefits can be included in the health scheme and how comprehensive these benefits will be while simultaneously maintaining affordability for plan sponsors. Determination of who is eligible for coverage is a major factor in this particular challenge. Also, as mentioned previously, very often a precise coding list of what is covered is not available. The absence of a standard coding list makes it very difficult to determine if a claim reflects a service that should be covered by the insurance scheme. This, in turn, makes the determination of a claim’s status subjective, and thus harder to predict and control.

Background on the health insurance microinsurance scheme

The development of the health insurance microinsurance scheme (health scheme) is in response to recent legislation to establish a health scheme to provide access to quality and affordable healthcare for all state residents in the African region. The goals of this program are to be affordable, sustainable, customer-centred and easy to understand and administer.

This scheme is eventually intended to be mandatory for the entire state population. However, at the start of this assignment, it was assumed that enrollment in the inception phase would start with a smaller population. The State MoH envisioned three scenarios for the healthcare package. In all scenarios, the recommendation was to include a comprehensive package covering primary care, maternity care, infant immunisations and referral services. Coverages for chronic care and specific diseases were priced on a modular (i.e., add-on) basis. The inclusion of dental and mental care was initially discussed with the MoH, but due to cost and affordability constraints, was not in the scope of the assignment. Ultimately, the MoH decided to include dental services in the package.

Two policies are anticipated to be available for purchase: an individual and a household policy. The household policy covers the main member, spouse and up to four children younger than 18 years old. For households exceeding a specified number of children, coverage for additional children is available.

Tailoring of projections for a specific population

PharmAccess has experience with two other health insurance schemes in Africa. However, these programs provide coverage for populations with demographic characteristics and health conditions that are anticipated to be significantly different than the population to be covered by the health scheme.

In the analysis, we spent significant time in understanding the demographic, cultural and health status differences between the various populations in order to ensure that we made the appropriate adjustments in the pricing model. For example, in one of the health insurance projects in which PharmAccess delivered technical assistance, there is significant skewing of the demographics in the population as well as specific influences leading to adverse health status. In reviewing the projections for the state population, we worked with PharmAccess to adjust the historical experience to more appropriately reflect the demographics and health status of the health scheme population based on factors such as access to care, differences between rural and urban regions and usage of traditional medicine.

As another example, we learned that in certain populations, there remains a large concern around giving birth in a hospital–a factor which can have a significant impact on the assumed birth rate at medical facilities. We also learned that in parts of Africa, there is very limited availability of insulin, which affects treatment protocols for individuals with diabetes type I.

In developing the projected premium for a household, we considered that households in the state can often be composed of two females and a number of children. Therefore, in the insurance pricing scheme, we considered a risk-mitigating provision where the number of maternal deliveries would be limited to one per year per contract.

Throughout the development and refinement of the health insurance pricing model, we worked concertedly to ensure that the projections appropriately reflected the anticipated population, health status, treatment patterns and specific cultural influences in the state in Africa. As many of these characteristics will be specific for each population, it was critical to ensure that PharmAccess’s projections made appropriate provisions for each anticipated population characteristic.

Consideration of affordability and risk-mitigating provisions

As a new insurance scheme in a developing nation, affordability was a key concern of the state government. As a part of the analysis, PharmAccess compiled statistics on the average household income of the anticipated population. In considering the affordability test, our team referenced the affordability provision in the US Patient Protection and Affordable Care Act (ACA). In the US, a premium greater than 9.5% of household income is considered “unaffordable.” Because the health scheme is a new program, it was helpful to be able to reference the US affordability test as a starting point for the analysis.

In the health scheme projections, we also considered the potential impact of risk-mitigating provisions. In the US, health payers often use (demand-side) member cost sharing as a part of insurance programs. For example, members will often pay a deductible, coinsurance or copay for certain types of medical services. The use of such member cost-sharing provisions is helpful in discouraging unnecessary utilization. For example, individuals may decide to wait to obtain care for minor illnesses (which may resolve without medical care) if they are required to share the cost for these treatments.

On the other hand, in many European nations, demand-side cost sharing1 is much less common and considered socially undesirable. Affordability and accessibility of good basic healthcare are cornerstones of many European healthcare systems and to control healthcare expenditures, supply-side cost-sharing mechanisms2 are therefore preferred.

In the health scheme, the state government determined that demand-side cost-sharing provisions would not be appropriate for a new program. Even though the long-term goal of the health scheme is mandatory coverage for the entire state population, the initial limited coverage of the program creates the potential for anti-selection, especially in the first years of the program.

Milliman’s microinsurance pricing model

Milliman’s microinsurance pricing model served as a key component of our actuarial review. Milliman developed this pricing model in order to provide a replicable framework for microinsurance projects as these types of analyses are relatively new in the developing world. As the health scheme is a new program for the anticipated population, there was limited data for many of the key utilisation statistics. PharmAccess has delivered technical assistance to other insurance schemes in Africa, and data from these programs was used as the starting point for the development of some of the key utilisation and cost projections.

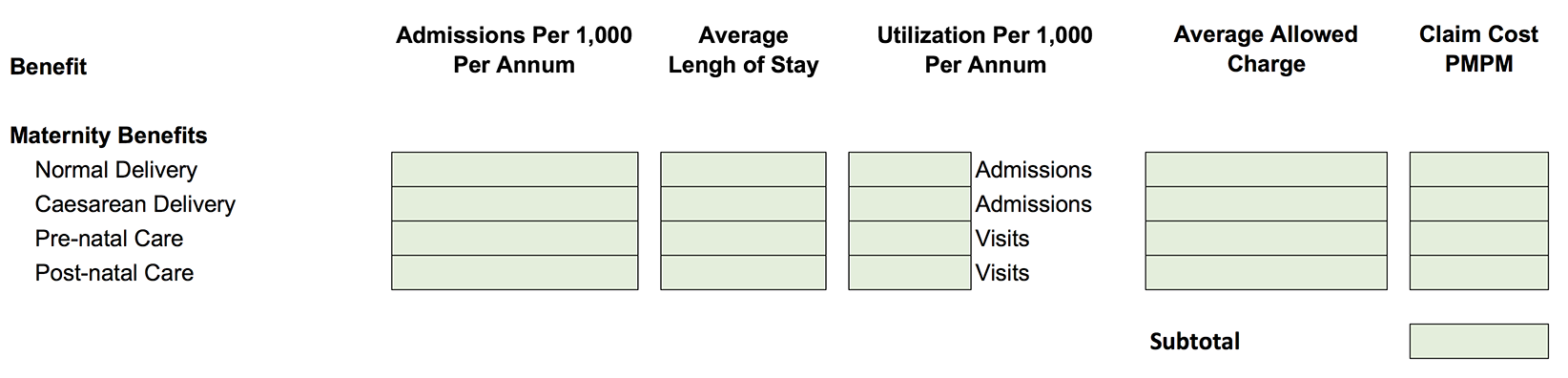

The Milliman team adapted the microinsurance pricing model for this specific analysis. In developing this model, we were able to use a structured approach to translate data and assumptions from PharmAccess consistently across each benefit component. The original pricing tool claim cost model is illustrated in Table 1A. In particular, we decomposed the utilisation statistics in order to provide greater visibility into the specific assumptions, which assisted our team with actuarial and reasonableness reviews.

Table 1a: Health insurance microinsurance scheme claim cost model

(Taken from Milliman's microinsurance model)

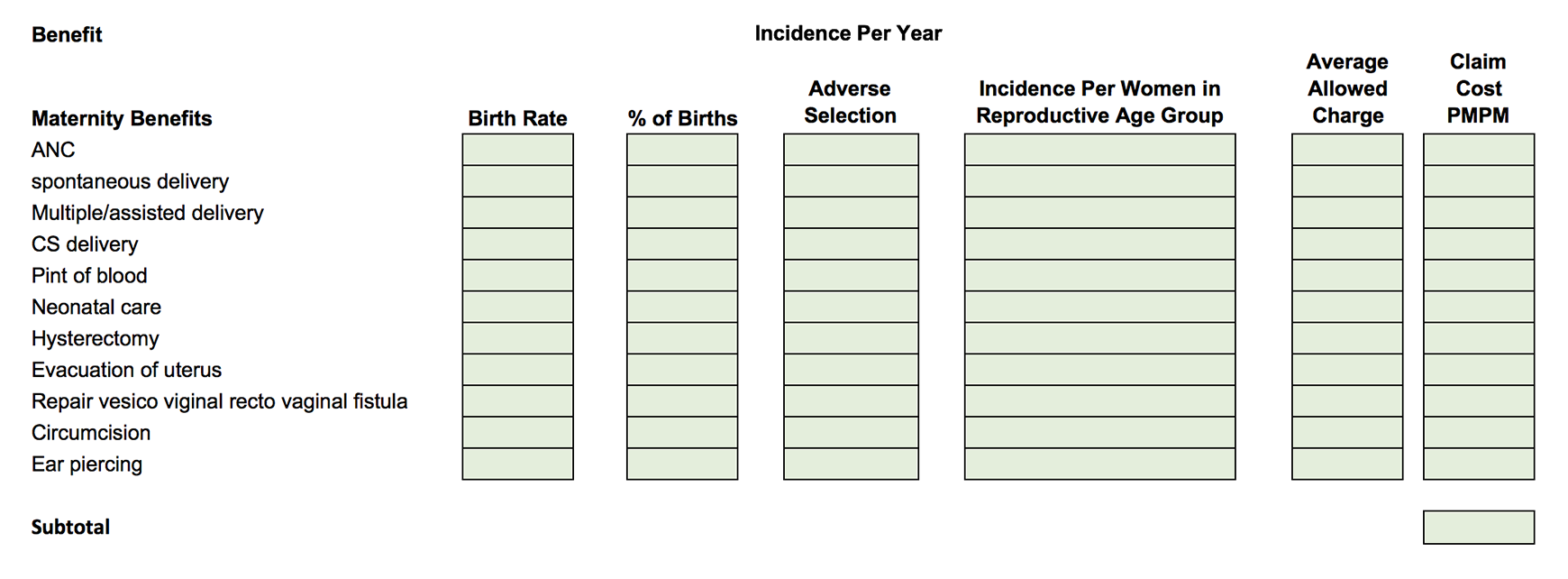

For example, for the maternity category of services, PharmAccess provided data with more specificity than simply deliveries and non-deliveries; we adapted the pricing model in order to explicitly show the total number of anticipated deliveries as well as a breakdown of the anticipated services to be provided as illustrated in Table 1B.

Table 1b: Health insurance microinsurance scheme claim cost model

(Taken from Milliman's microinsurance model)

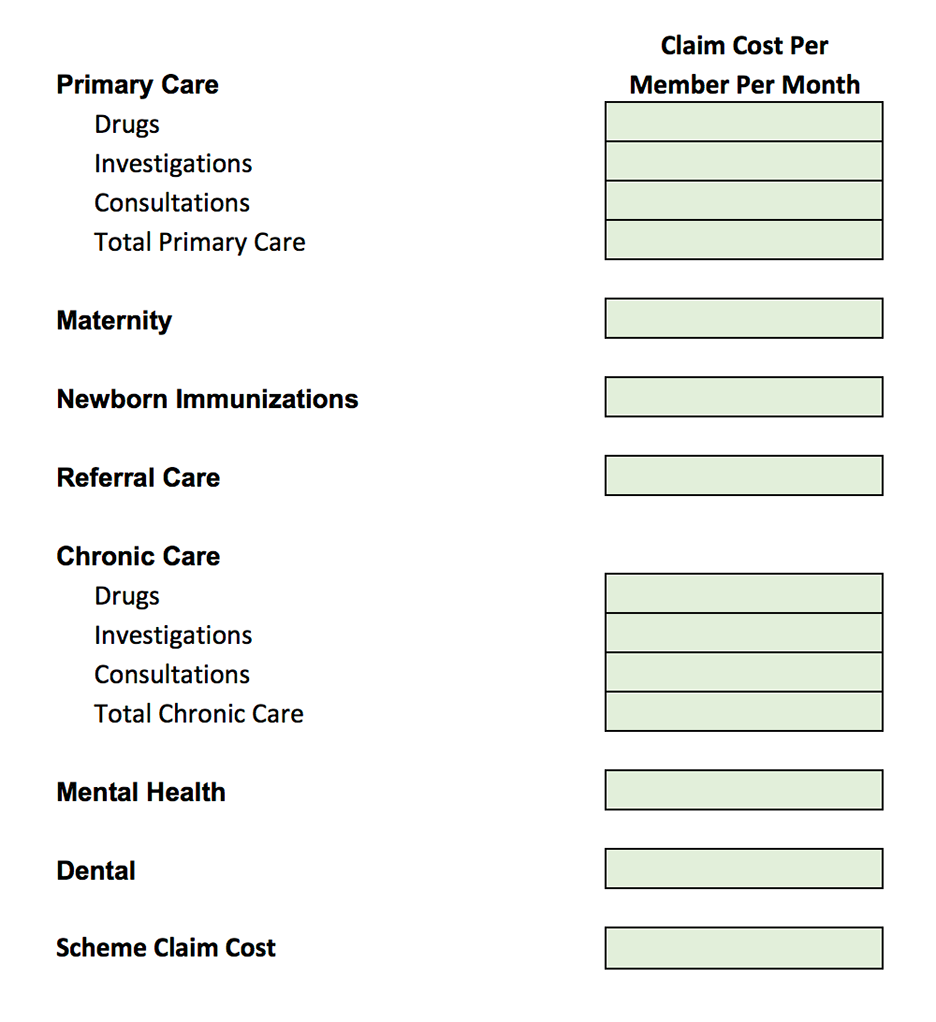

We also adapted the pricing model to reflect the specific premium composition anticipated for the health scheme as illustrated in Tables 2 and 3.

Table 2: Health insurance microinsurance scheme summary

Individual policy premium rate development

Table 3: Health insurance microinsurance scheme summary

Household policy premium rate development

Furthermore, the pricing model was adapted to be able to sensitivity test important pricing assumptions, including data credibility, age and gender adjustments, inflation and trend, and provider discounts and network usage.

Lessons learned

Strength of an international, cross-disciplinary team

Milliman brought together an experienced team composed of actuaries and clinicians from several countries. Due to the specialised nature of the project, it was critical to involve senior consultants in the in-depth reviews of the actuarial and financial projections as well as a detailed review of the clinical assumptions.

Dr. Lalit Baveja and Dr. Sudhanshu Bansal, clinical consultants from Milliman’s New Delhi office, contributed their extensive expertise gained from prior microinsurance projects. In developing regions, there is often significant variation in the prevalent medical conditions, provider treatment patterns, available technology, use and availability of prescription drugs and numerous other factors which influence medical utilisation and costs. The in-depth clinical review was critical in Milliman’s review of the underlying assumptions in the health insurance pricing scheme costs.

Milliman’s team included several actuaries from the United States and the Netherlands: Lynn Dong, Susan Pantely, Briana Botros and Judith Houtepen. The team combined its expertise from medical insurance programs and worked closely with PharmAccess’s team to perform an in-depth review of the actuarial pricing assumptions.

Milliman’s Health Cost Guidelines (HCGs), the US industry gold standard for medical pricing, forms a strong basis for most health insurance pricing analyses. Although the utilisation and costs for health services vary from those in the US, the methodology and cost projection methodology are similar to those used in the US. The team considered many of the principles from the HCGs in the analysis: utilisation and cost statistics; the impact of varying demographics and health status characteristics; likelihood of anti-selection in a new insurance program; potential impact of risk-mitigating provisions (cost sharing, waiting periods, etc.); and development of premium categories (individual, household, etc.).

A key takeaway from the health scheme project is that an international, interdisciplinary team with broad clinical and actuarial expertise is key to the success of a microinsurance analysis. Because there is often limited data available for new microinsurance schemes, it is critical to involve experts who can provide insight and feedback into the specific issues likely to affect the overall health benefit costs for a specific region and population.

Visibility of Milliman’s involvement

Due to the political sensitivities surrounding the project, it was essential for PharmAccess that the state government understood that Milliman was closely involved in this project. Even though we were not directly involved with the state government and PharmAccess was our client, our review role was made clear in various ways. First, in the Statement of Work between PharmAccess and the state government, Milliman’s role in reviewing the pricing assumptions was explicitly mentioned. Furthermore, in the final report from the NGO, it was explicitly mentioned that Milliman was retained by the NGO to assist with the review of the medical premium development for the health scheme and that we summarised our findings regarding assumptions, key considerations, limitations and caveats in a cover letter to PharmAccess. And lastly, our presence during the final presentation was regarded as critical by PharmAccess. Because Milliman’s physical attendance at the final presentation was not feasible, PharmAccess preferred to hold the final presentation via a video conference (in which Milliman participated).

Interaction between PharmAccess and the state government

An important component of the project was the interaction between PharmAccess and the state government. PharmAccess is headquartered in the Netherlands and has local offices in Kenya, Tanzania, Ghana and Nigeria. There is added value in working in conjunction with representatives from PharmAccess to leverage local experience and connections with the stakeholders. This type of project is often surrounded by political sensitivities, which makes local presence even more important. In addition, throughout the project, the PharmAccess consultant made several trips to Africa in order to present the preliminary results and receive feedback from the state government. The state government partnered with PharmAccess to provide advice on the health scheme. However, the final decision remained with the MoH.

An effective collaboration

Milliman was proud to collaborate with PharmAccess on this microinsurance analysis. Key to Milliman’s mission statement is protecting the health and financial well-being of people everywhere. The health scheme, by endeavouring to provide affordable health insurance to a population in a developing region which was previously not covered by insurance, fits well within Milliman’s mission statement.

Milliman’s international team of actuaries and consultants, as well as Milliman’s microinsurance pricing tool, contributed significantly to the success of this project. We look forward to partnering with other organisations on microinsurance projects and to continuing our work to improve the health and financial well-being of people everywhere.